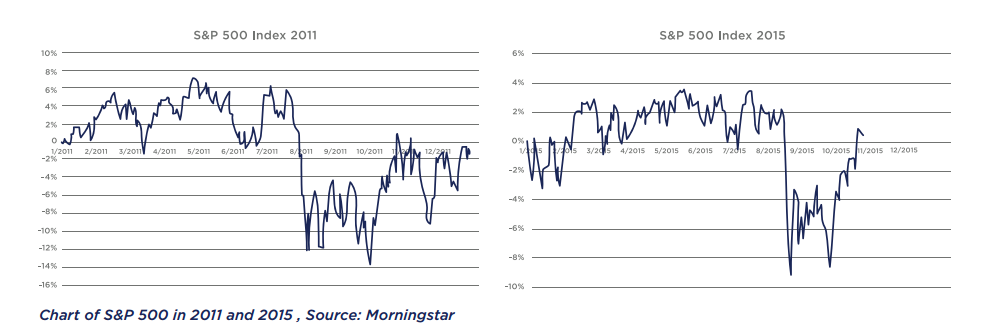

This Too Shall Pass (Or Has Passed?)

Almost ten months into 2015, market performance this year reminds me a lot of 2011. The S&P 500 ended that year at 1257.60, fractionally off the 1257.64 level where it ended 2010. The Wall Street Journal stated, “For the S&P 500, 2011 Basically Never Happened.” But 2011 was a painful series of advances, declines, a near bear market decline of 19.4%, and a bumpy recovery to end the year flat. For investors, 2011 was emotionally trying even if nothing really happened.

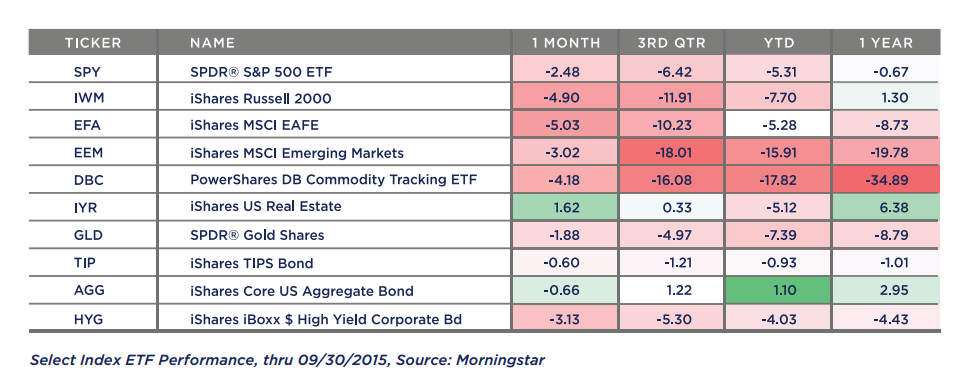

While not quite as turbulent, this year has been interesting to say the least. 2015 started off near all-time highs and advanced slowly, but steadily until May. From May through early August the market essentially stalled, until the tail end of the third quarter rolled in with gale force winds. The most often cited market index, the S&P 500 ended down about 6.4% for the quarter which erased the gains achieved earlier in the year and even brought the trailing twelve month return into negative territory. Small cap stocks, international stocks, emerging market stocks, and most commodities fell even further. Bonds were the only traditional asset class that saw positive returns with the Barclays Aggregate Bond Index posting a meager 1.3% for the quarter and 1.0% for 2015.

So how did we weather this storm? We pride ourselves on outpacing the market in periods of stress such as these. Our most over-weight position in all portfolios was US equity exposure. We have long favored larger capitalization, higher quality, low volatility stocks. The iShares MSCI US Minimum Volatility ETF is our preferred proxy. This ETF was down only 1.3% for the quarter (vs the S&P down 6.4%). While we had exposure to both international and emerging markets stocks, security selection (again focusing on low volatility positions) added about 5% relative to the traditional benchmarks (MSCI EAFE Index and MSCI Emerging Markets Index).

These low volatility strategies we employ tend to underperform slightly when the markets roar upwards, but earn their keep when the going gets tough. Most clients also had exposures to two strategies that we rely on in difficult times that seek to provide returns that are not dependent on stock or bond indices moving upwards. The first was a trend following strategy managed by AQR. This fund was up more than 6% in the quarter. The second is a new holding to portfolios that capitalizes on various arbitrage opportunities. This fund was up a modest 1.6% in the quarter, but we are very excited to have added it to our roster of investment options.

We manage market risk in several ways. The first and most basic is diversification—that is, not putting all of one’s eggs in a single basket. Traditional diversification had very little effect on performance for the quarter with most international assets dropping more than their domestic counterparts. Bonds were a saving grace with a positive 1.2% return for the quarter, but most long term investors were underweight bonds going into the quarter because of their low (2% or so) yields and correspondingly low expected longer run returns. We also seek to further diversify a portfolio beyond a traditional stock and bond mix. We spend a lot of time researching strategies that are not dependent on rising equity markets or falling interest rates. Many of these strategies were significant contributors for the quarter. An additional way we seek to mitigate the drawdowns that can occur in periods like this is to look for strategies that have demonstrated outperformance in down markets.

Our outlook has not changed much from our last newsletter. US stocks are still more expensive than their long run average. This reflects a consensus view of a stable, if not strong, domestic economy. However, higher than average valuations suggest that future returns will likely be below the long term average. Foreign stocks and emerging market stocks have been relatively cheap and have gotten cheaper as concerns over China’s economic strength have rattled the global economy. In the long run these low valuations portend higher future returns. Bond yields are now around 2% for the 10 year treasury. Historically the yield on the 10 year treasury is a pretty good guide to the future 10 year return on bonds. While this likely means that bonds will not be providing the same strongly positive base for portfolio returns in the next ten years that they were for the last 10 plus years, we will still expect them to provide stability to portfolios and a boost when economies and markets trip. Commodities have struggled mightily since the price of oil started to tumble in the fall of 2014. The Bloomberg Commodity Index, a widely used benchmark representative of broad commodities recently hit levels not seen in almost 20 years. This is largely attributable to a slowing global economy. But as an old saying goes, the best thing for low commodity prices is low commodity prices. We can see direct evidence of this as global oil demand hit an all-time high last month.

As has been the case with all of the newsletters I’ve written in the past year, market sentiment changed quickly and October has ushered in strong gains. The S&P 500 is again positive for the year and markets appear to have settled back into an uptrend. While this is quite positive in the short-term, I am left wondering what is driving prices to act so manically. Underlying economic fundamentals certainly do not have 15% swings in a matter of weeks. I am curious too if such short-lived market declines can have the positive, cleansing effects that traditional bear markets had flushing weak hands and excesses from the global markets over the course of many months.

We continue to focus our research efforts on finding strategies and opportunities that will protect capital in difficult markets while still offering attractive return potential in the long-run.

As always, it is important that clients think through their goals and circumstances and communicate any issues or changes to us.

DISCLOSURES:

This presentation is not an offer or a solicitation to buy or sell securities. This presentation may not be construed as investment advice and does not give investment recommendations. Any opinions included in this report constitutes the judgment of Signal Ridge as of the date of this report and are subject to change without notice.

The investments presented are examples of the securities held, bought and/or sold in Signal Ridge strategies during the last 12 months. These investments may not be representative of the current or future investments of those strategies. You should not assume that investments in the securities identified in this presentation were or will be profitable. We will furnish, upon your request, a list of all securities purchased, sold or held in the strategies during the 12 months preceding the date of this presentation. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of securities identified in this presentation. Signal Ridge, or one or more of its officers or employees, may have a position in the securities presented, and may purchase or sell such securities from time to time.

Additional information, including management fees and expenses, is provided on Signal Ridge’s Form ADV Part 2. As with any investment strategy, there is potential for profit as well as the possibility of loss. Signal Ridge does not guarantee any minimum level of investment performance or the success of any portfolio or investment strategy. Past performance is not a guarantee of future results.