Q4 2023 Investment Update

Summary

- The beginning of Q4 saw a continuation of the challenging conditions seen in Q3 as bond yields, represented by the 10yr Treasury bond, continued their upward march touching 5% intraday in mid-October

- That trend reversed course and then accelerated following Fed Chairman Powell’s comments on 12/13 after the latest FOMC meeting

- Chair Powell acknowledged the likelihood of rate cuts in 2024, aiming to avoid being too restrictive for too long

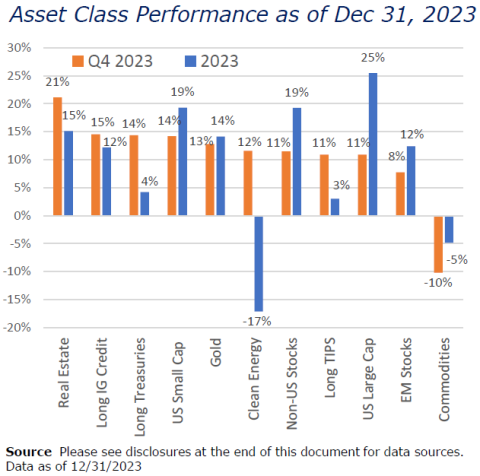

- This spurred strong performance for both stocks and bonds for the quarter while commodities sold off

A Dovish Pivot

For the majority of 2023, several financial market themes carried over from 2022, specifically the Fed’s objective to get inflation back down to its 2% target by pushing interest rates higher. The Fed raised rates by 4.25% in 2022 and another 1% in 2023 before pausing after its most recent July hike. And while interest rates on longer dated securities such as Treasury bonds are determined by buyers and sellers in the market, rates – or “yields” – also continued their march higher. The yield on the 10yr Treasury bond in March 2022 just before the Fed began raising rates was 1.83%. That yield hit 4.1% following the Fed’s July hike and peaked at just under 5% towards the end of October. Bond yields and prices have an inverse relationship, which meant bond prices fell significantly over this time.

However, at the December 13th meeting of the Federal Open Market Committee (FOMC), Chairman Jerome Powell acknowledged in his press conference that the market is pricing in rate cuts in 2024 and did not push back on that possibility. This was interpreted as a dovish pivot by the Fed Chair, or a potential inflection point where the Fed shifts from a more restrictive monetary policy to one that may be more accommodating. That apparent signal was a welcome surprise for both stock and bond markets.

It was a strong bounce back year for US equities, led by mega tech names such as NVIDIA, Meta, and Amazon. And while it was a positive year for Treasury bonds – both nominal and inflation-linked – it was the Fed’s December dovish pivot that drove their returns for the year into positive territory. Bonds remain well below their highwater mark set in August 2020 following historically strong performance in the earlier days of the pandemic.

Commodities ex gold and commodity stocks fell during the quarter leading to a loss for the year after a strong 2022. Higher rates intended to slow the economy typically have a downward effect on commodities as the demand for raw materials pulls back.

Surveying for Lag Effects

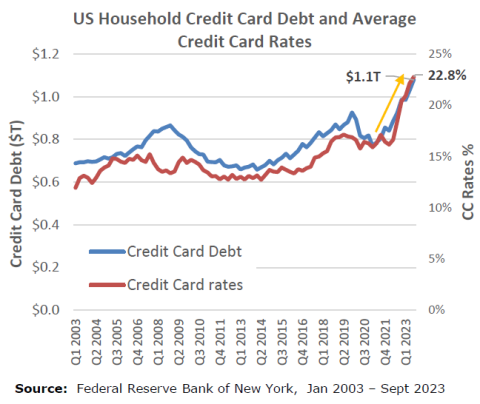

The Fed Funds rate is a typical starting point used to determine the interest rate on a range of lending activities, such as credit cards and adjustable-rate mortgages. Whereas bond yields in the 5-, 7-, and 10-year range are more relevant to interest rates on car loans and fixed-rate mortgages. Collectively, we have seen a significant rise in the cost of borrowing, most acutely felt with credit card balances and new mortgages. Consumers’ capacity to take on more debt is stretched as we, as a country, have never been more indebted and credit is the most expensive that it’s been over the last 20 years.

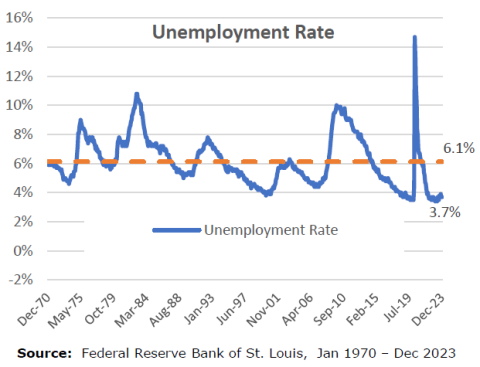

Often, tighter conditions result in a rise in unemployment, which contributes to slowing inflation. During the Great Inflation of the 1970’s and early 80’s, unemployment peaked at 10.8% in 1982 before falling steadily over the next seven years. Today, unemployment remains near historic lows at 3.7%. As central banks raise interest rates in response to an overheated economy, consumers and businesses begin to feel these higher borrowing costs. Consumers tend to spend less, which puts pressure on business profitability, which can cause businesses to reduce costs in the form of layoffs. Employees are one of the largest costs for any given company. And while we saw 2023 layoff announcements from the likes of Nike, Intel, GM and more, it has done very little to meaningfully move the unemployment rate. The below graph shows that rate since 1970 along with the average over that period.

It is unclear whether a rise in unemployment is still to come or if there will be a rekindling of inflation. The Fed is attempting to avoid both, which has been a notoriously difficult thing to do for central banks faced with these conditions.

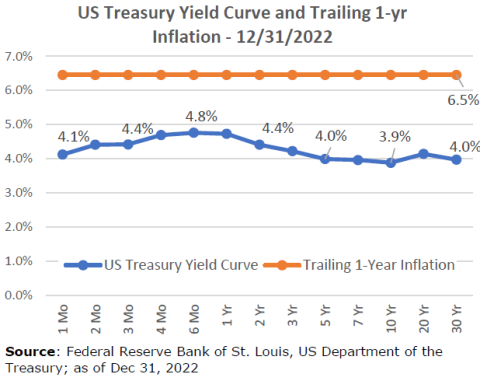

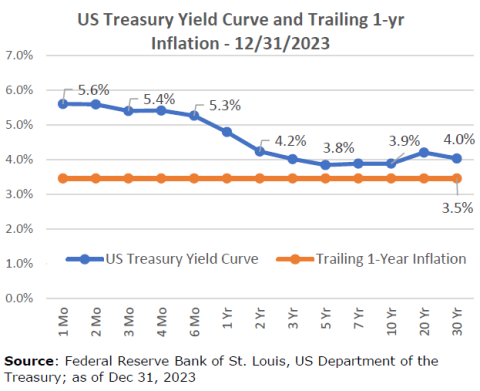

Fed Chairman Jerome Powell acknowledged that we’ve made good progress on inflation with the trailing 1-year headline Consumer Price Index (CPI) now sitting at 3.5%. Importantly, all parts of the Treasury yield curve now sit above the inflation rate. This is important because investors holding bonds at any duration today project to earn a positive “real” return, or a return above inflation. The below two charts show the US Treasury Yield Curve along with trailing 1-year inflation, the first as of 12/31/22 and the second as of 12/31/23.

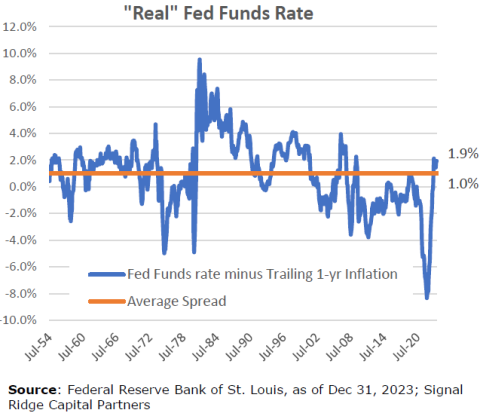

Lastly, applying this to the Fed Funds rate, the average spread relative to trailing 1-year inflation has been 1%. Today it sits at 1.9%. Taking this picture altogether, it has given the Fed confidence to change their tone while still recognizing it will be a meeting to meeting exercise to determine where its policy rate will go next.

Stocks and bonds tend to move together when inflation is the more dominant economic condition. That was true in 2022 when both suffered significant losses. And as inflation has started to ease both have begun to recover together.

Financial Markets and Election Years

While politics and markets are undeniably linked in many ways, financial markets tend to track underlying fundamental economic conditions, opportunities and risks most closely. Monetary policy, as set by the central bank, is an apolitical function and tends to have a more persistent and direct effect on financial markets. On the other hand, fiscal policy and other government-related budgetary decisions very much have partisan influences and will shift left and right depending on the party composition of the House, Senate and Oval office. While this election is setting up to be even more politicized and divisive than the last one, the below data provide some insight into financial markets during election years to see if there are any historical trends that may inform what we might expect for 2024.

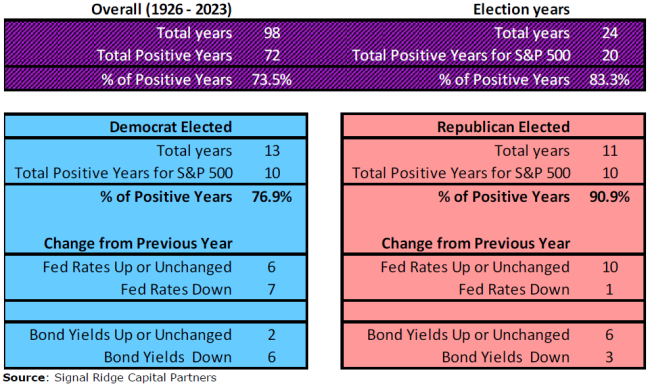

Since 1926 we have had 24 elections. Equity markets – as measured by the S&P 500 – have registered a positive return in 20 of 24 (83%) of those years, which compares to a 73% rate over all years since 1928. From a party perspective, years in which Democrats were elected the S&P 500 was up 77% of the time, whereas Republican-elected years the market was up a notable 91%. The GOP favors lower taxes and less regulation, both of which skew towards a more stimulative economic environment.

Conversely, interest rates – both base rates set by the Fed as well as bond yields as determined by the market – have tended to be up in election years that resulted in a Republican victory. Pointing to the challenge of higher rates and the campaign promise to deploy more stimulative policies can be appealing to the American voter from a GOP perspective. Years in which Democrats were ultimately elected have leaned more towards lower rates. Democrats tend to skew towards higher taxes and tighter regulation. Rates trending down – economically stimulative – has perhaps eased one of the concerns of the American voter when considering the Democratic candidate.

Ultimately, we believe it will be the economic conditions that matter most that will drive financial markets in 2024. Despite the favorable numbers during election years, it is worth remembering that 2008, an election year in which the Great Financial Crisis unfolded, saw the S&P 500 drop -37%. The bursting of the Tech Bubble happened in 2000, another election year. The S&P 500 dropped -9% that year and went on to fall -12% in 2001 and -22% in 2002. Regardless of who was elected to office that year, it was a housing crisis (2008) that drove the GFC and ‘irrational exuberance’ (Alan Greenspan), as well as by a terrorist attack and accounting scandals that fueled the 2000 downturn. From our perspective, while the data may favor a positive year, we believe the underlying economic conditions matter more. And we stand firmly behind the merits of building diversified portfolios with the goal of avoiding risk concentration to help us better navigate whatever may lay ahead in 2024.

Important Disclosures and Data Sources

The following indices and securities were used to represent the performance of various asset classes contained in this market commentary:

- US Large Cap stocks – S&P 500 Index; Standard & Poor’s

- US Small Cap stocks – Vanguard Small-Cap Index Fund ETF, which seeks to track the performance of the CRSP US Small Cap Index that measures the investment return of small-capitalization stocks

- Non-US stocks – iShares Core MSCI EAFE ETF, which seeks to track the investment results of the MSCI EAFE IMI Index composed of large-, mid- and small-capitalization developed market equities, excluding the U.S. and Canada

- Emerging Market stocks – iShares Core MSCI Emerging Markets ETF, which seeks to track the investment results of the MSCI Emerging Markets Investable Market Index

- Real Estate – real estate returns are represented by the FTSE Nareit U.S. Real Estate Total Return Index Series

- Long Duration Investment Grade Credit – Vanguard Long-Term Corporate Bond Index Fund ETF, which seeks to track the performance of the Bloomberg U.S. 10+ Year Corporate Bond Index

- Long Duration US Treasuries – iShares 20+ Year Treasury Bond ETF, which seeks to track the investment results of the ICE U.S. Treasury 20+ Year Bond Index (the "underlying index")

- Long Duration US TIPS – PIMCO 15+ Year U.S. TIPS Index Exchange-Traded Fund, which seeks to provide total return that closely corresponds, before fees and expenses, to the total return of the ICE BofA 15+ Year US Inflation-Linked Treasury Index

- Gold – World Gold Council, https://www.gold.org/goldhub/data/gold-prices

- Commodities – iShares S&P GSCI Commodity-Indexed Trust, which seeks to track the results of a fully collateralized investment in futures contracts on the S&P GSCI Total Return Index

- Clean Energy - iShares Global Clean Energy ETF , which seeks to the investment results of the S&P Global Clean Energy IndexTM composed of global equities in the clean energy sector

Important Disclosures

Past performance does not guarantee future results. It is not possible to invest in an index. Performance shown for the SRCP Aggressive model represents an unaudited, asset weighted composite of actual client returns, net of all management fees and before advisor fees, as calculated by the custodian, Charles Schwab. Individual account performance may vary based on inception date of the account, timing of rebalancing, trade execution prices, timing of cash flows, fees, taxes and other potential factors. All views and opinions expressed in this letter are solely those of Signal Ridge Capital Partners, are subject to change at any time without notice, and are not a recommendation to buy or sell any securities.

Signal Ridge Capital Partners is registered investment adviser, CRD No. 167576