Q1 2024 Investment Update

Summary

- Q1 saw a continuation of the equity momentum seen in Q4 with rate cut expectations being confirmed by Fed Chairman Jerome Powell

- However, January and February’s CPI prints showed stagnation in the Fed’s efforts to bring inflation back down to its 2% target

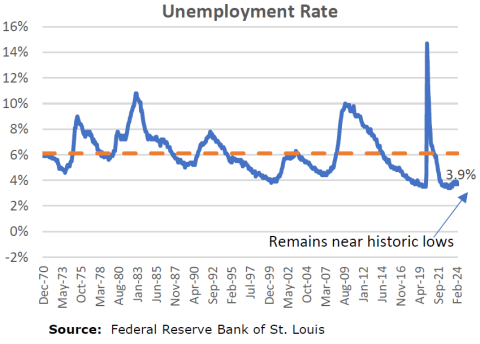

- Coupled with historically low unemployment and rising consumer sentiment, market expectations around potential cuts took a more hawkish shift, weighing on interest rate sensitive sectors such as bonds and real estate

The Optimism Continues

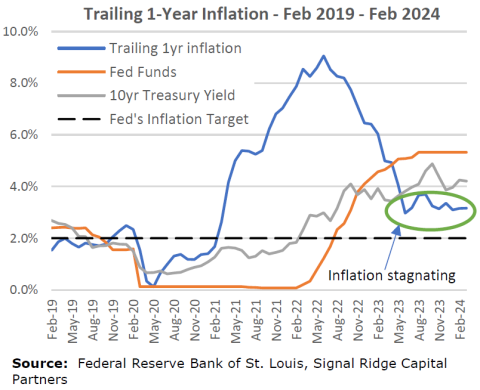

Over the course of the 1st quarter optimism around a soft landing continued driven by the Federal Reserve confirming that rate cuts would be forthcoming in 2024. Beginning in Q4 2023 when the Fed pivoted to a more dovish tone, there has been speculation in the marketplace around how many cuts and when those cuts may begin. At the Fed’s March meeting, Chairman Jerome Powell confirmed that he anticipated three rate cuts this year in order to bring the Fed’s “real” rate back into neutral territory from its current restrictive level. On average, the Fed has kept its base policy rate about 1% above of inflation. Through February, the trailing 1-year inflation rate was 3.2% with the Fed’s policy rate sitting in the range of 5.25-5.50%, suggesting some room to cut.

As the Fed carefully considers its next move, they are processing a wide range of data in realtime that can influence policy. And while there has been steady progress on inflation from its 2022 recent peak, January and February’s CPI readings of 0.5% and 0.6%, respectively, were significant enough to renew concerns that the Fed’s inflation fighting efforts are not finished. The unemployment rate remains near historical lows and US equity markets have shown great resilience in the face of rising rates, suggesting that the Fed doesn’t need to be in a hurry to reverse course. At present, the US Treasury yield curve implies that Fed will make its first cut of 0.25% in June.

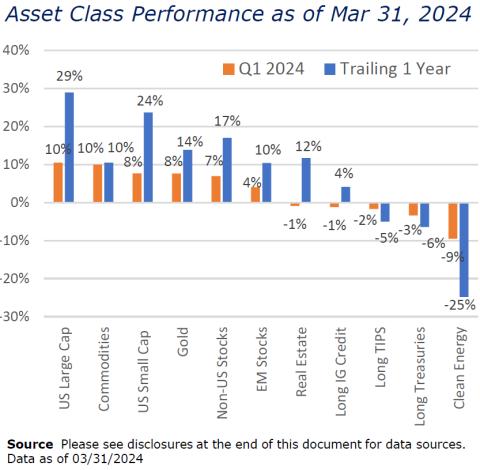

From a markets perspective, the development of artificial intelligence (AI) has far and away been the biggest driver of equity market optimism. Conversely, the recent pick-up in the CPI again weighed on bonds and other interest-rate sensitive sectors such as real estate and clean energy.

While the forward-looking inflation path and its effect on interest rates will continue to contribute to elevated volatility in the bond market, we feel more confident that the worst of what can rightfully be called a bond crisis is behind us, at least from a performance perspective. And while bonds have weighed on performance over the last two years, certainly stocks have been the biggest driver. Other diversifying asset classes such as gold and managed futures have served as meaningful contributors.

These non-equity contributions are important as we think about the benefits of diversification. It is tempting to develop a perspective that the current environment is the environment that will persist indefinitely, that stocks will always be the primary money-making asset class and the bond market will continue to be a drag. There is ample financial history to provide insight into periods where stocks struggled and bonds were a critical positive contributor. The bursting of the Tech Bubble in 2000 and the Great Financial Crisis of 2008-09 are the most notable examples in recent times. However, predicting when that type of environment will return can be a challenging game.

Current conditions appear to be relatively stable despite what has been one of the Fed’s most aggressive rate hiking cycles in its history, an environment that would typically be followed by a recession. So far, that recession has thankfully not arrived.

Checking in on Current Conditions

Beginning below we’ve provided an update on three notable macro indicators: the latest inflation rate along with both short and long-term interest rates, the unemployment rate, and finally the latest reading from the University of Michigan Consumer Sentiment Index, a measure of consumer confidence.

The preceding chart shows trailing 1-year inflation along with the Fed Funds rate, the 10- year US Treasury yield and the Fed’s long-term inflation target. The good news is that both the Fed Funds rate and 10yr bond yield are above the current trailing one year inflation rate. However, that rate remains above the Fed’s long-term target and has not moved lower since June 2023. That also happens to be when the Fed last raised its base rate. They continue to expect lag effects to bring the inflation rate down further, though those effects have yet to materialize. With this as the current set up, it’s not surprising that the Q4 stock and bond market optimism for rate cuts was tempered in Q1.

To be clear, a low unemployment rate is a good thing, though the Fed’s maximum employment mandate is more nuanced. The Fed aims to achieve the maximum level of employment that can be sustained without overt inflationary pressure, which it defines as 2%, on average. Since 1970, the unemployment rate has averaged 6.1%, well above the current rate of 3.9%. While the Fed will never say it wants the unemployment rate to rise – which can create hardship for individual families – it knows an increase would help cool the economy and there is capacity for that to happen. An unemployment rate that remains this low will continue to be a headwind to achieving its price stability mandate.

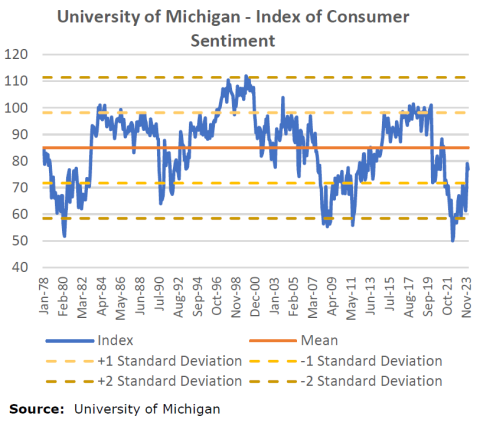

In the middle of 2022, consumer confidence was as low as it had been at any point in the last 45 years. As the Fed paused its rate hikes and economic growth continued to be positive, confidence grew that we might avoid a recession and achieve the ever allusive “soft landing”. While we are still below the mean sentiment level, both consumers and economists alike are getting more confident that we will avoid a significant economic downturn following this unprecedented period of rate hikes.

Looking Ahead

As we move further into 2024 there is no shortage of current events that have the potential to sway the economic landscape. At the geopolitical level, the US continues to fight two proxy wars, supporting both the Ukraine’s fight against Russia and Israel’s fight against Hamas. On the former, the Biden administration continues its efforts to provide military aid to the Ukraine, despite pushback from the Republican-controlled House. On the latter, in the post WW II era no country has received more military aid than Israel, an indication of the strength of the bond between the two countries. Recently, however, that bond has come under pressure as the US has become increasingly uncomfortable with how Israel has conducted its operations in Gaza. Both wars continue without a clear catalyst for an end. In the meantime, these tensions have put upward pressure on oil prices – which have now risen almost 20% year-to-date – while lives continue to be lost.

The US presidential election now sits approximately seven months away with the real political mudslinging yet to begin. As referenced in the previous quarterly letter, election years tend to be good ones in financial markets. Circumstances matter, however. Both 2000 and 2008 were election years and both saw equity market losses, the latter on a historical scale. An orderly election cycle would be to the benefit of all involved, regardless of the outcome.

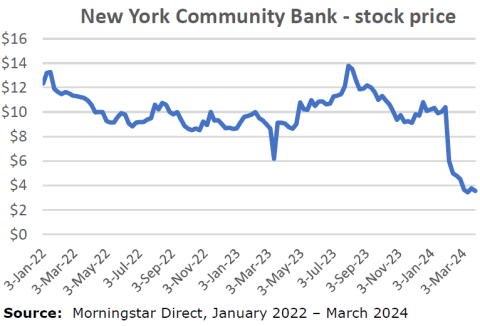

At the micro level, the recent events surrounding New York Community Bank (NYCB) are perhaps just as concerning from an investment perspective as any of the geopolitical conditions. Just over a year ago, NYCB bought insolvent Signature Bank, which had a high degree of uninsured deposits and loan exposure to the volatile cryptocurrency industry. A year later, NYCB itself was on a path to insolvency due to significant loan losses in its commercial real estate portfolio in the New York City area.

Since then, the CEO has been replaced and the bank has been rescued by a group of outside private investors led by former Treasury Secretary Steve Mnuchin. While we hope this is not the canary in the coal mine, we remain on the lookout for any stress that may be percolating from this higher interest rate environment.

As always, thank you for your continued partnership with Signal Ridge Capital Partners as we aim to navigate these uncertain times. Should you have any questions, please do not hesitate to reach out.

Important Disclosures and Data Sources

The following indices and securities were used to represent the performance of various asset classes contained in this market commentary:

- US Large Cap stocks – S&P 500 Index; Standard & Poor’s

- US Small Cap stocks – Vanguard Small-Cap Index Fund ETF, which seeks to track the performance of the CRSP US Small Cap Index that measures the investment return of small-capitalization stocks

- Non-US stocks – iShares Core MSCI EAFE ETF, which seeks to track the investment results of the MSCI EAFE IMI Index composed of large-, mid- and small-capitalization developed market equities, excluding the U.S. and Canada

- Emerging Market stocks – iShares Core MSCI Emerging Markets ETF, which seeks to track the investment results of the MSCI Emerging Markets Investable Market Index

- Real Estate – real estate returns are represented by the FTSE Nareit U.S. Real Estate Total Return Index Series

- Long Duration Investment Grade Credit – Vanguard Long-Term Corporate Bond Index Fund ETF, which seeks to track the performance of the Bloomberg U.S. 10+ Year Corporate Bond Index

- Long Duration US Treasuries – iShares 20+ Year Treasury Bond ETF, which seeks to track the investment results of the ICE U.S. Treasury 20+ Year Bond Index (the "underlying index")

- Long Duration US TIPS –PIMCO 15+ Year U.S. TIPS Index Exchange-Traded Fund, which seeks to provide total return that closely corresponds, before fees and expenses, to the total return of the ICE BofA 15+ Year US Inflation-Linked Treasury Index

- Gold – World Gold Council, https://www.gold.org/goldhub/data/gold-prices

- Commodities – iShares S&P GSCI Commodity-Indexed Trust, which seeks to track the results of a fully collateralized investment in futures contracts on the S&P GSCI Total Return Index

- Clean Energy - iShares Global Clean Energy ETF , which seeks to the investment results of the S&P Global Clean Energy IndexTM composed of global equities in the clean energy sector

Important Disclosures

Past performance does not guarantee future results. It is not possible to invest in an index. Performance shown for the SRCP Aggressive model represents an unaudited, asset weighted composite of actual client returns, net of all management fees and before advisor fees, as calculated by the custodian, Charles Schwab. Individual account performance may vary based on inception date of the account, timing of rebalancing, trade execution prices, timing of cash flows, fees, taxes and other potential factors. All views and opinions expressed in this letter are solely those of Signal Ridge Capital Partners, are subject to change at any time without notice, and are not a recommendation to buy or sell any securities.

Signal Ridge Capital Partners is registered investment adviser, CRD No. 167576